🚨 Twin Debt Crisis: Student Loans and Auto Payments Set to Detonate Consumer Credit

America's credit engine is seizing—and it's doing so on two fronts. Student loan delinquencies are rocketing back post-repayment freeze. Auto loan defaults are accelerating to recession-level highs. Together, they paint one unmistakable picture: a consumer credit system nearing critical overload. Welcome to the next financial inflection point.

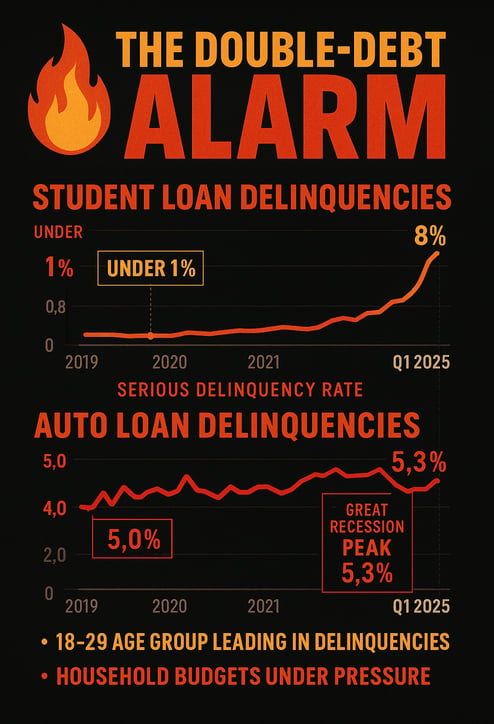

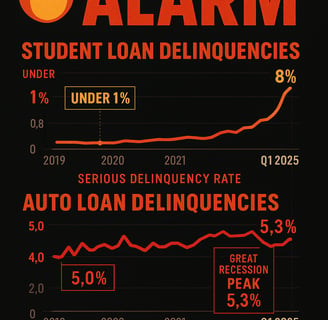

🔥 The Double-Debt Alarm

Student loans? A powder keg. In Q1 2025, serious delinquencies jumped from under 1% to nearly 8% in just three months. This isn’t a bump—this is a spike, driven by the end of pandemic-era relief and the cold restart of loan collections.

Auto loans? Equally volatile. 5.0% of borrowers are now 90+ days late—just shy of the Great Recession peak of 5.3%. The younger the borrower, the higher the risk: the 18–29 demographic is leading the surge in auto defaults.

What’s fueling this twin firestorm? One word: pressure. Household budgets are squeezed. Wages have stagnated. Inflation cooled on paper but not in the grocery aisle, gas pump, or loan statement. Add record-high interest rates and you've got a population that's leveraged to the edge—and slipping.

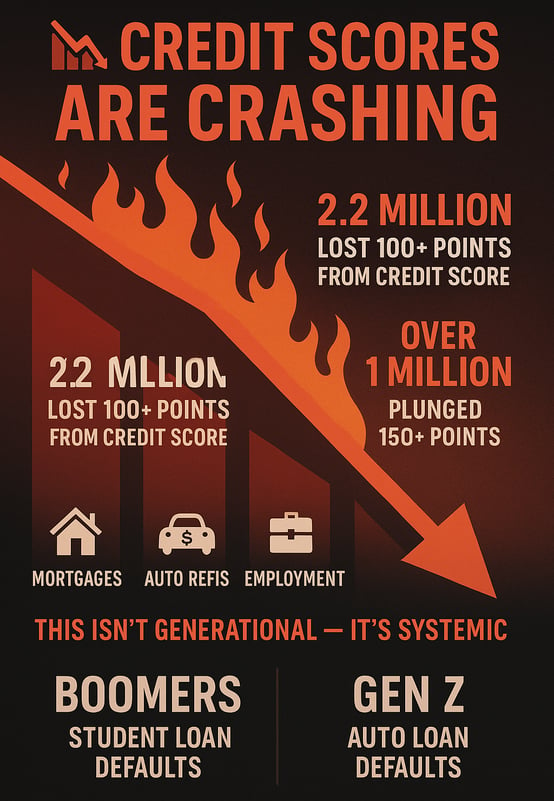

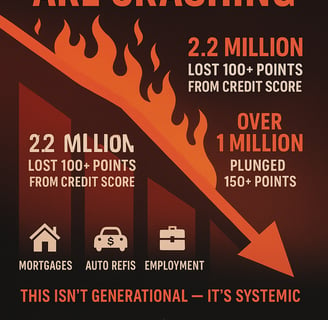

📉 Credit Scores Are Crashing

The fallout is brutal. 2.2 million Americans have lost 100 or more points from their credit scores since January. Over one million have plunged by 150 points or more. This isn’t just a ding—it’s a collapse in creditworthiness. It shuts doors to mortgages, auto refis, and even job opportunities.

Boomers are defaulting on their student loans. Gen Z is defaulting on their cars. This isn’t generational—it’s systemic.

📊 The Forecast: Convergence = Crisis

Let’s break it down:

Auto loan delinquencies will likely surpass their 2010 peak by mid-2026.

Student loan defaults among older borrowers are already at crisis-era highs.

When both breach the 3.5% threshold simultaneously—as current data suggests—we enter what analysts call a “twin-peak” event: a rare, violent phase of credit stress seen only in deep recessions.

The implications? Massive. Credit underwriting will tighten. Subprime lending will contract. Auto sales will dive. Repossession rates will soar. And downstream industries—insurance, manufacturing, retail—will feel the aftershock.

⚙️ What Comes Next

This is not a waiting game. The signs are here now.

Banks must recalibrate risk models—yesterday.

Automakers should prepare for suppressed demand and inventory bottlenecks.

Regulators and legislators? You’re on the clock. Targeted student debt relief isn’t political anymore—it’s structural. If you don’t act, the defaults will.

🧨 Final Word: Time’s Up

This isn’t about watching trends. This is about reading signals. Student debt and auto loans are not isolated bubbles—they’re coiling together. And when they blow, they’ll hit every corner of the economy.

Ignore the noise. Watch the defaults. Prepare for impact.