The Auto Loan Crisis: How Young Americans Are Crushed by Debt

Auto loan delinquencies are skyrocketing, and no one’s talking about the real problem. Young buyers are drowning under sky-high car prices, stagnant wages, and a system that’s stacked against them. With student loans, rising rents, and no relief in sight, this isn’t irresponsibility—it’s survival.

Ladies and gentlemen, it’s time we had an honest conversation about auto loan delinquencies in America. You’ve seen the headlines: “Delinquencies are rising!” “Consumers are falling behind!” “Wall Street is worried!” But as usual, the media and the so-called “experts” are missing the point. They’re laser-focused on the immediate numbers, regurgitating soundbites without any understanding of what’s really going on.

Let me tell you the truth: This isn’t just about late payments. This is about a broken economy that’s crushing young borrowers, a bloated auto market drunk on its own hype, and a system rigged to squeeze every last dollar from consumers. And yes, it’s about how today’s borrowers have options that didn’t exist before, options that are reshaping the way we think about car ownership.

Young Borrowers: The Generation Crushed by Debt and Unforgiving Timing

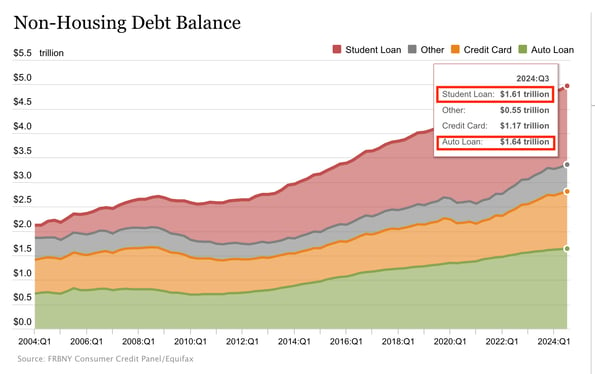

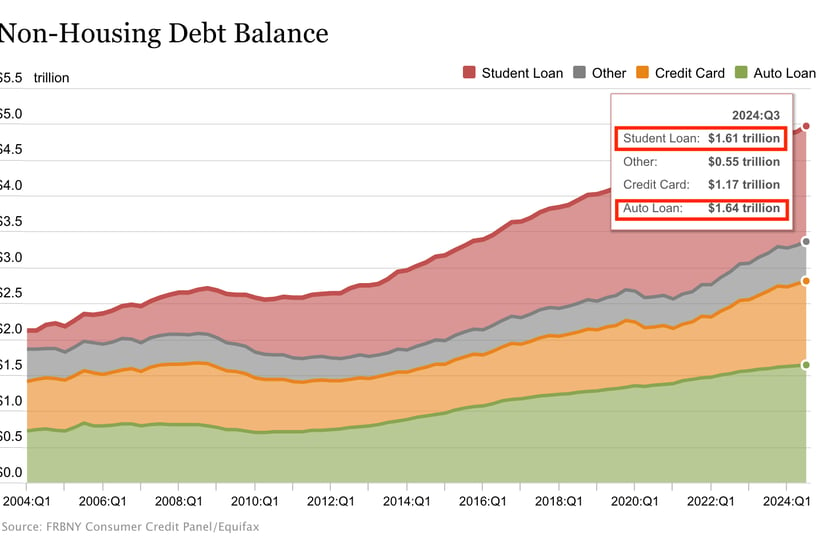

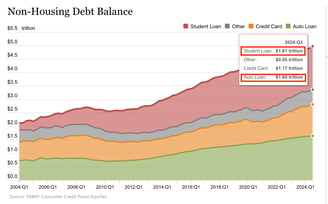

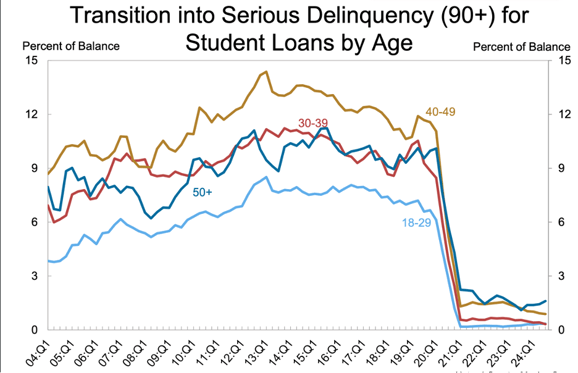

Let’s start with the group that’s bearing the brunt of this mess: younger buyers. Delinquencies are skyrocketing among borrowers aged 18–39, and the reasons go far beyond personal responsibility. This generation is stuck with the short end of every stick—outrageous car prices, higher interest rates, stagnant wages, and now the return of student loan payments, thanks to the Biden administration’s end to the repayment pause. It’s a perfect storm, folks, and they’re right in the eye of it.

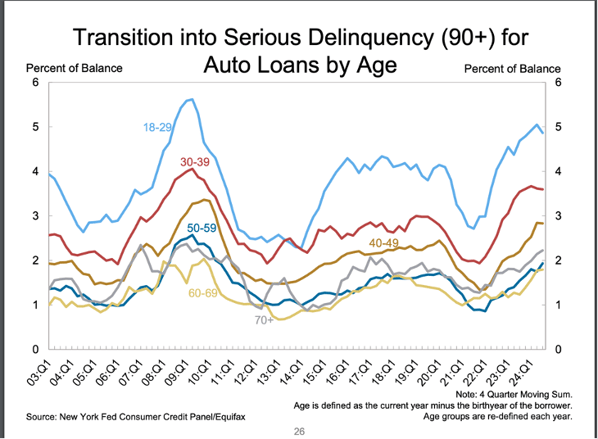

Take a look at the data. The sharpest increases in delinquency rates are happening in the 18–29 and 30–39 age groups. And why wouldn’t they? These are the same borrowers trying to manage student loan payments that just resumed after a three-year reprieve. Pair that with a shaky economy where inflation is still eating away at paychecks, and you’ve got a generation that’s drowning before they’ve even had a chance to swim.

And here’s the thing: when you’re paying $700+ a month for a car, $400 for student loans, and still trying to afford rent and groceries, something has to give. For many, it’s the car payment.

The Student Loan Factor: A Ticking Time Bomb

Here’s what no one wants to admit: The restart of student loan payments is the catalyst that could tip this entire situation into crisis territory. Before the pandemic, these payments were already a massive burden. Then came the pause, giving borrowers some breathing room. But now? The payments are back, and the timing couldn’t be worse.

You’ve got an economy teetering on uncertainty, with layoffs creeping into white-collar jobs and inflation keeping household budgets tight. Student loans are essentially squeezing younger borrowers from one side, while auto loans squeeze from the other. And let’s be clear—this isn’t just a problem for them. When this many borrowers fall behind, it’s going to ripple through the entire economy.

The Auto Market’s Pressure Cooker

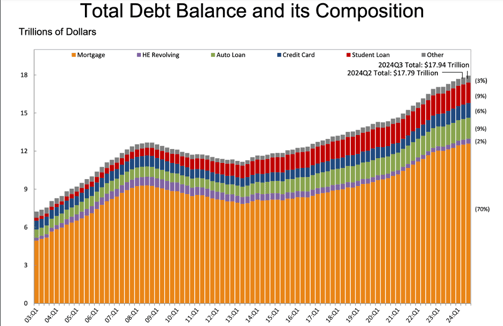

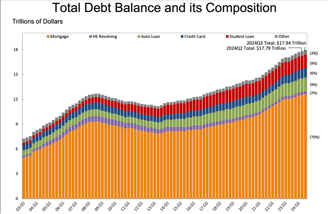

Now, add the auto market to this equation. Younger borrowers aren’t just dealing with student loans; they’re dealing with car payments that are higher than ever before. New car prices are through the roof, and used car prices, even post-pandemic, remain inflated. The loans they took out in 2021 and 2022 came with record-high interest rates, locking them into payments that are barely manageable, even in the best economic conditions.

And let me remind you—back in 2008, when borrowers fell behind on car payments, they didn’t have many options. No car meant no job, plain and simple. But today’s borrowers have a safety net: rideshare services like Uber and Lyft. It might sound insane to use Uber daily, but when you can’t afford your car note, it’s a lifeline. Back then, repossession meant financial ruin. Now, it’s a painful inconvenience, but not the death sentence it used to be.

The Auto Market: Overpriced and Out of Touch

Now, let’s talk about the auto industry itself—because they’re not blameless here. For years, automakers have been squeezing supply, driving up prices, and pretending like this is all normal. Used car prices are still way above pre-COVID levels, and new cars? Forget about it. Automakers are pricing their vehicles like every buyer has Tesla money.

The problem isn’t just the sticker prices. It’s the loans. Today’s loans are longer, with bigger monthly payments, locking buyers into deals that stretch their budgets to the breaking point. Interest rates are climbing, and those higher rates are hitting borrowers where it hurts the most—their wallets.

And who’s making bank off this mess? Wall Street. Subprime auto loans backed $40 billion in securities this year, up 17% from 2023. Investors are betting big that consumers will somehow keep paying for overpriced cars, even as delinquencies rise. Let me tell you, folks—this isn’t a business model; it’s a house of cards.

The Delinquency Panic: Why This Time Feels Different

Now, let’s get to the heart of the matter. Yes, delinquencies are climbing. In fact, 4.4% of auto loans are now over 90 days delinquent—the highest level since 2021. And yes, it’s easy to sound the alarm. But here’s the thing: We’ve been here before.

Remember 2020? Delinquencies spiked back then, too. Everyone panicked, but the numbers eventually pulled back. The difference this time is what’s happening in the broader economy.

White-collar job cuts are piling up. Tech companies are laying off workers. More and more industries are trimming their salaried employees. This isn’t just an issue for hourly workers anymore—this is creeping into sectors that used to feel secure.

If those job cuts continue, delinquencies won’t just level off. They’ll surge. And once that happens, the domino effect will start: repossessions, credit score hits, and even tighter lending standards. It’s a vicious cycle, and we’re standing on the edge of it right now.

The Bottom Line

Auto loan delinquencies are more than just a statistic. They’re a symptom of a broken system—one that’s crushing young borrowers, overpricing essentials, and gambling on a future that looks increasingly unstable.

The next time you read another think piece blaming delinquencies on consumer irresponsibility, remember this: It’s not the borrowers who are irresponsible. It’s the automakers, the lenders, and the investors who’ve rigged the game.

Mark my words: This isn’t going to end with a whimper. If the job cuts continue, if the prices stay this high, and if Wall Street keeps playing roulette with the economy, the fallout will be felt by everyone.

So, wake up, folks. Stop believing the headlines. Start asking the real questions. Because if we don’t, the next financial crisis might be pulling into the driveway sooner than we think.

The Looming Economic Shockwave

Folks, here’s the bottom line: this situation is more than just a rise in delinquencies. It’s a warning sign of a much bigger problem. If student loan repayments and auto debt keep squeezing younger borrowers, they’ll cut spending elsewhere. That means less money flowing into other parts of the economy. And when layoffs pick up—and trust me, they will—it’s going to accelerate.

This isn’t just a hiccup. This is the system breaking down under its own weight. The younger generation is being crushed by policies and prices they didn’t create but are now being forced to endure. And let me tell you, folks, when this crisis hits full force, it’s not the borrowers who should be blamed. It’s the leaders, the experts, and the automakers who built this mess and turned a blind eye as it spiraled out of control.